Executive Summary

Ecommerce is no longer a growth story — it is the commerce story. The global market crossed $6 trillion in 2024, accounts for more than one-fifth of all retail sales, and is on a trajectory to reach $11–13 trillion by 2031. Yet the era of easy, double-digit growth is giving way to a far more demanding competitive environment.

Three forces are reshaping the landscape simultaneously: AI has moved from experimentation to expectation, powering personalization, logistics, and customer service at scale; social commerce is emerging as a primary sales channel, not a supplement; and mobile-first consumers, especially Gen Z, are rewriting the rules of discovery, trust, and conversion.

This report provides a data-grounded view of where the market stands today and a clear strategic roadmap for where your company must be positioned by 2031. The central finding is direct: businesses that commit now to five structural capabilities — AI-powered personalization, omnichannel integration, mobile-native experiences, trusted payments, and sustainable operations — will disproportionately capture the next wave of growth. Those that remain in optimization mode will face rapid commoditization.

| KEY FINDING | By 2031, ecommerce could reach $11–13 trillion globally. Social commerce alone is projected to exceed $6.2 trillion. Companies that do not build the foundational infrastructure today will not be able to compete in this environment at all. |

Section 1: The State of Ecommerce Today

1.1 Market Scale & Momentum

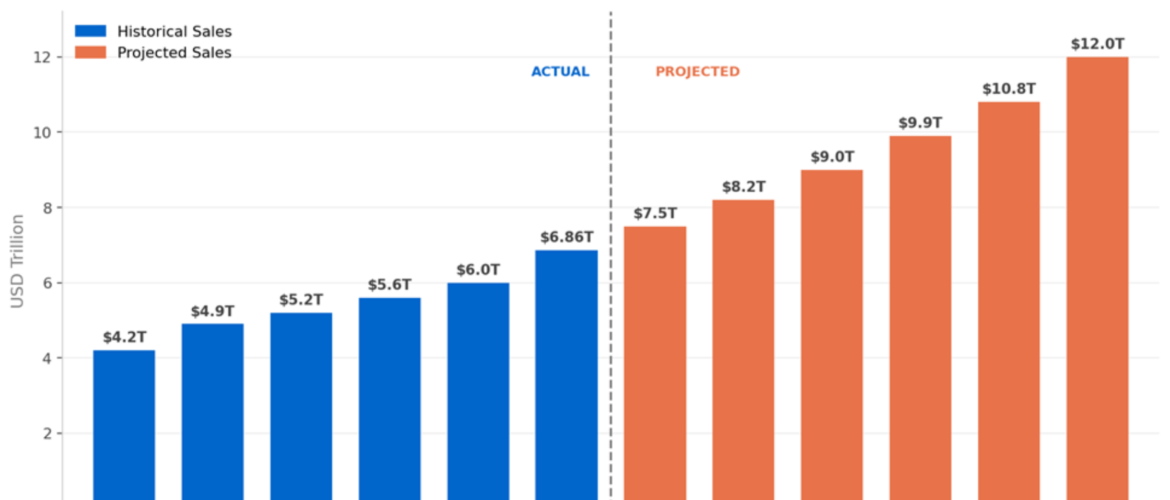

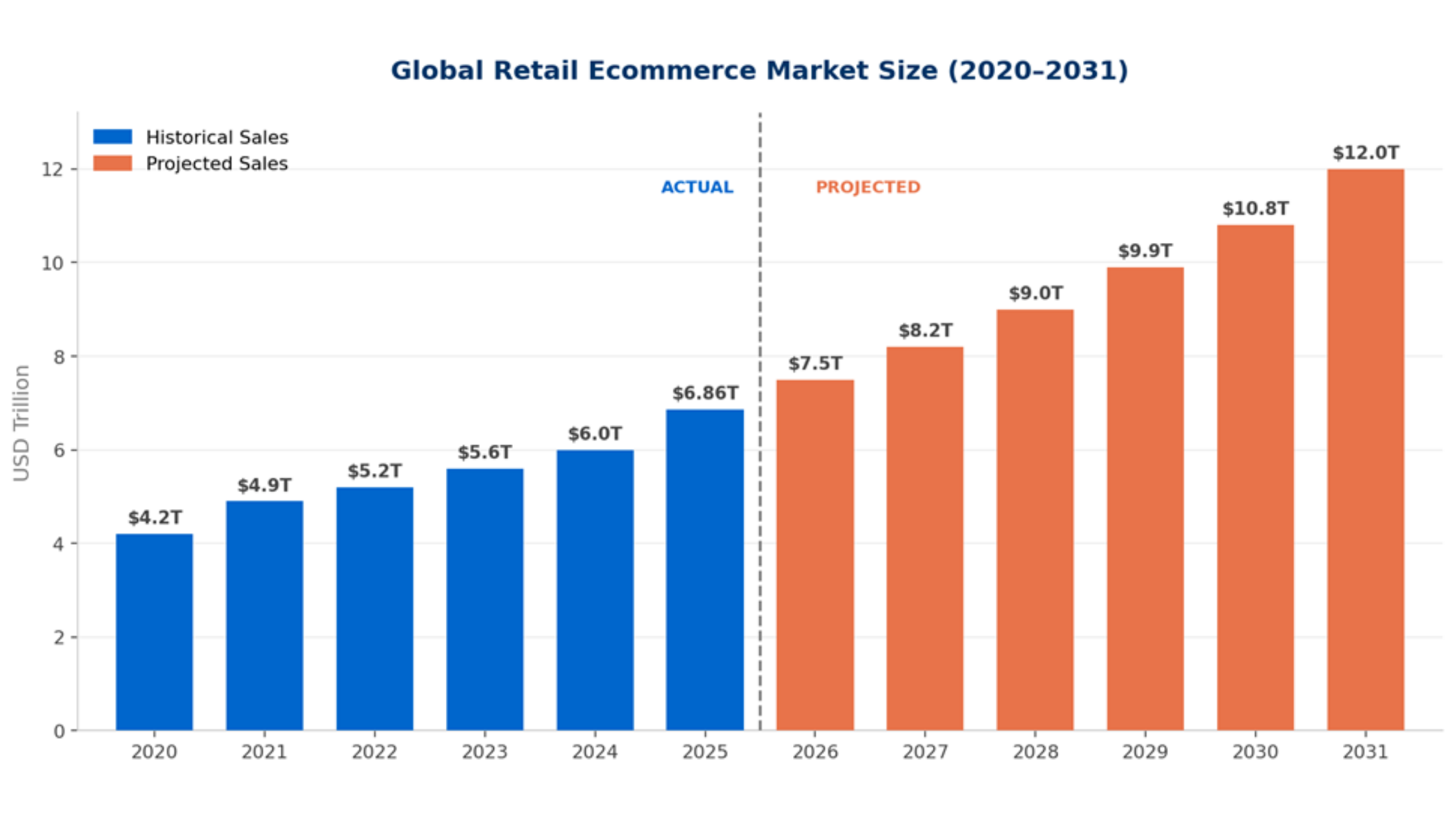

The numbers are unambiguous. Global retail ecommerce sales reached an estimated $6.0–6.4 trillion in 2024 and are expected to surpass $6.86 trillion in 2025 — an 8.4% year-over-year increase at a time when in-store retail is growing at only 3%. Ecommerce now represents approximately 20.5% of all global retail sales, up from 17% in 2022, and that share is projected to reach 27–30% by the end of the decade.

The United States and China together account for over $2 trillion in annual ecommerce volume. India and Southeast Asia are growing at more than 24% per year, making them the most important expansion markets of the decade. Mobile commerce — with 62% of all transactions now happening on smartphones — has effectively become the default interface for global online shopping.

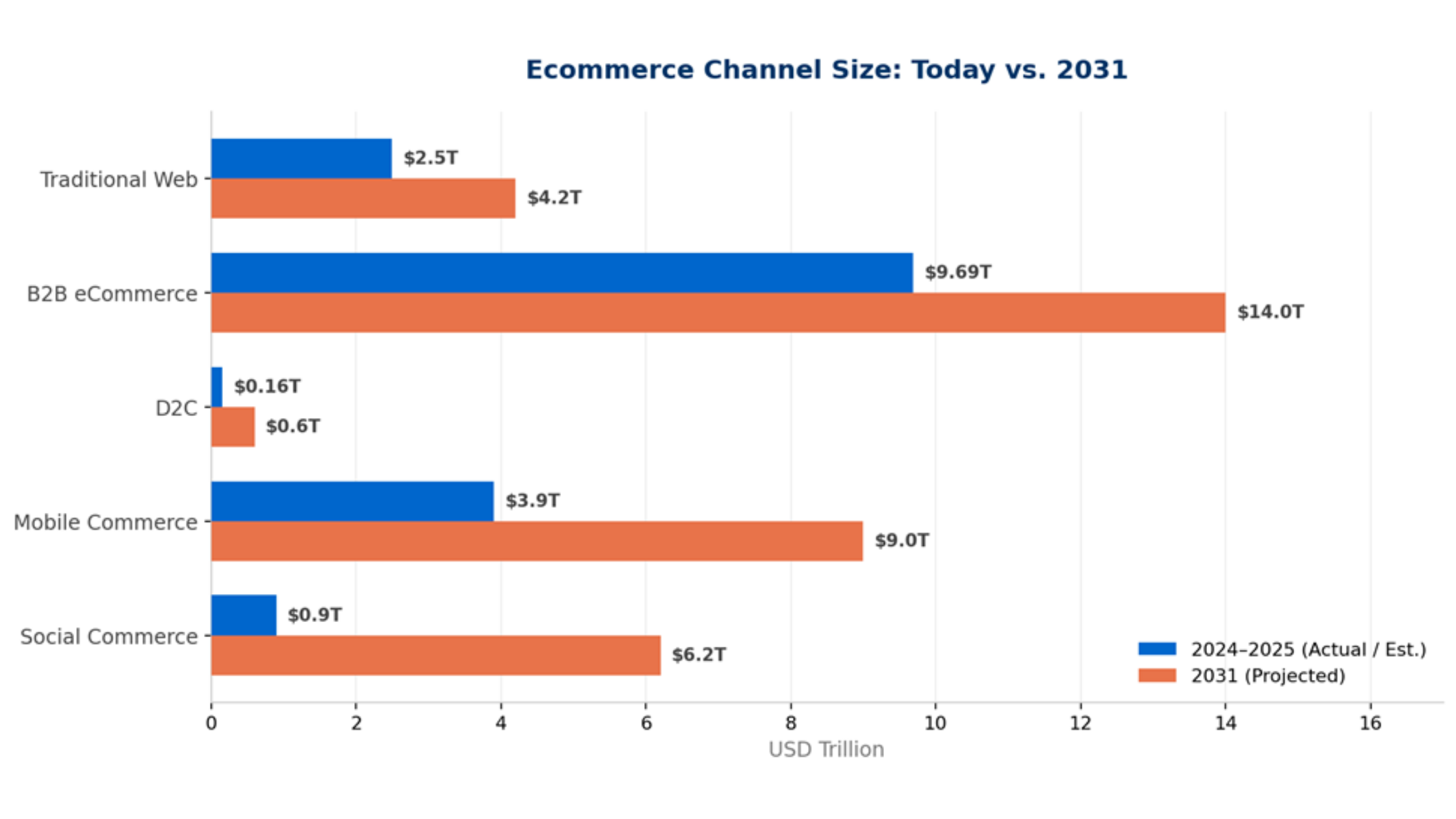

| Metric | 2024 (Actual) | 2025 (Estimate) | 2031 (Projected) |

| Global Retail eCommerce Sales | $6.0T | $6.86T | ~$11–13T |

| eCommerce as % of Global Retail | 17–20% | 20.5% | 27–30% |

| Global Online Shoppers | 2.64B | 2.77B | 3.8B+ |

| Mobile Commerce Share | 62% | 65%+ | 75%+ |

| Social Commerce Revenue | $0.9T | $1.2T+ | $6.2T+ |

| AI in eCommerce Market Size | $8.65B | $10B+ | $22.6B+ |

| B2B eCommerce (US) | $9.69T | $10T+ | $14T+ |

Sources: eMarketer, Statista, Shopify Enterprise Research, Shoptrial, SellersCommerce (2024–2025)

1.2 The Forces Driving Growth

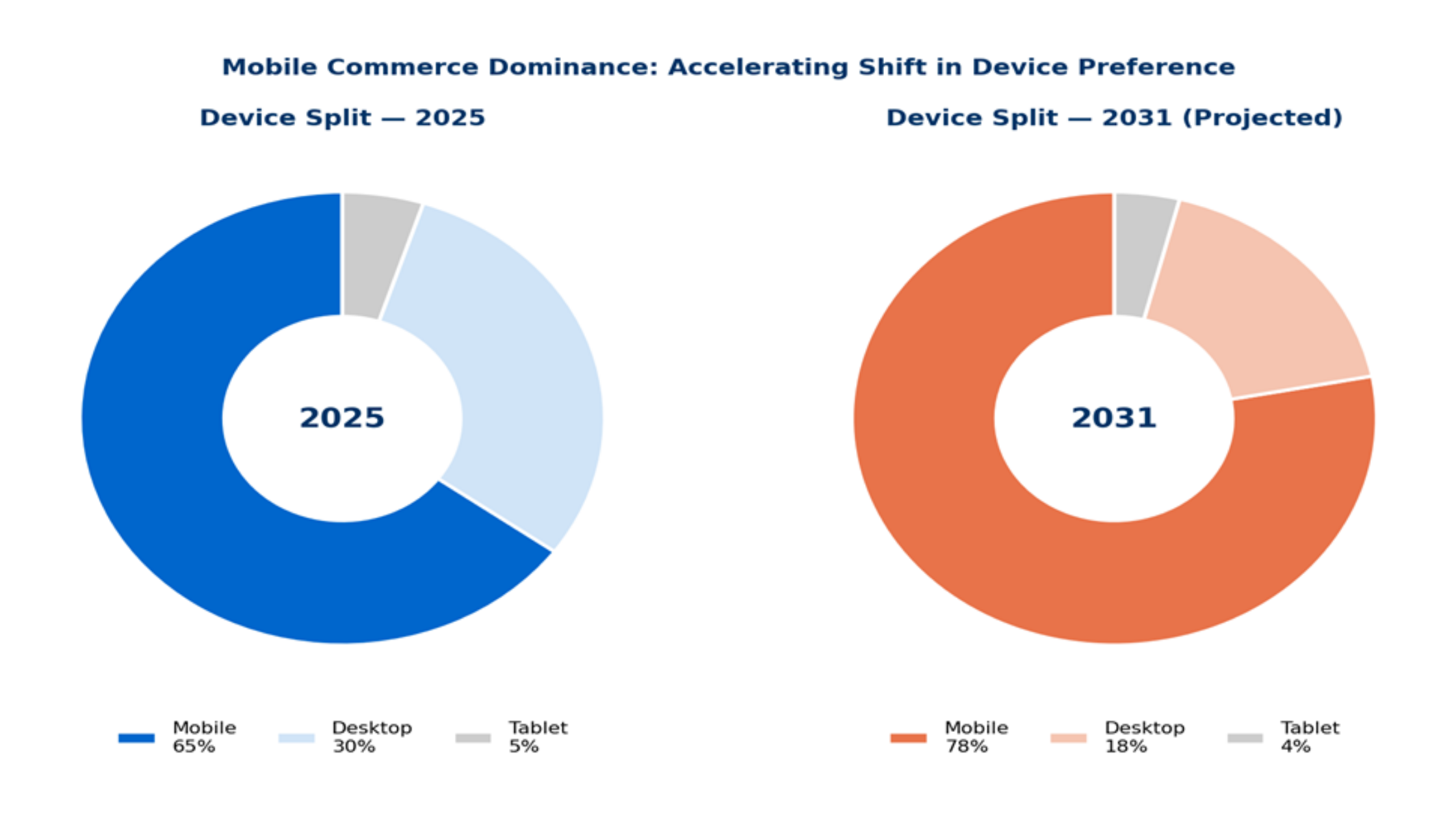

Mobile Commerce Dominance

More than 1.65 billion consumers shopped via mobile devices globally in 2024. In Asia, over 85% of all online transactions are now mobile-initiated. In the US, mobile commerce is expected to reach $900 billion in 2025, representing nearly half of all ecommerce sales. The practical implication: any company that does not have a mobile-native experience is already behind.

Social Commerce as a Primary Sales Channel

TikTok Shop contributed to 26% growth in US social commerce sales in 2024. Seven in ten global shoppers have already made a purchase via social media, and that same proportion expects social platforms to be their primary shopping destination by 2030. Social commerce revenue is projected to reach $6.2 trillion by 2030 — a figure that exceeds the entire global ecommerce market of just five years ago.

AI Becoming Infrastructure, Not Feature

51% of ecommerce businesses are already using AI to deliver personalized experiences. The AI-in-ecommerce market reached $8.65 billion in 2025 and is projected to hit $22.6 billion by 2032. Agentic commerce — where AI completes purchases on behalf of consumers — is moving from pilot to production. ChatGPT’s Instant Checkout feature, launched in September 2025, allows AI to execute purchases from over a million Shopify stores without a human ever opening a browser.

The D2C and B2B Convergence

The global D2C market reached $162.9 billion in 2024 and is projected to grow to $595 billion by 2033. Simultaneously, B2B ecommerce — often underestimated — generated $9.69 trillion in US sales alone in 2024, representing 86.6% of all US ecommerce. The boundaries between B2B and B2C buying behavior are dissolving as business buyers expect the same seamless, consumer-grade experiences.

| DATA POINT | By 2030, AI is projected to manage 80% of customer interactions in ecommerce. Companies leveraging AI see average revenue increases of 10–12%. This is no longer a competitive advantage — it is a baseline requirement. |

1.3 The Structural Challenges You Must Solve

Despite impressive growth, the ecommerce market is simultaneously becoming more complex and more commoditized. Three structural tensions define today’s operating environment:

- Discovery is fragmenting. Consumers start their shopping journeys across search engines, social media, apps, and AI assistants. No single channel commands majority attention. Maintaining visibility across all touchpoints requires radically different content, data, and budget strategies than three years ago.

- Trust and returns are eroding margin. With $849.9 billion in US returns forecast for 2025 — nearly 15.8% of online sales — return management has become a profitability crisis, not a logistics afterthought. Cybersecurity costs are expected to reach $10.5 trillion annually, making digital trust a board-level concern.

- Conversion efficiency is declining. Global conversion rates fell 1.86% in recent tracking periods, driven by inflation, experience fatigue, and rising consumer selectivity. Winning businesses are not just driving more traffic — they are engineering every step of the purchase journey to remove friction.

Section 2: The Five-Year Outlook — 2026 to 2031

The next five years will not be a linear continuation of the past five. They will be defined by platform convergence, the normalization of AI-native commerce, and the redistribution of consumer attention and wallet share to whoever best combines trust, speed, and personalization. The following are the five macro-shifts that will determine competitive outcomes.

Shift 1: AI Becomes the Operating System of Commerce

By 2031, AI will not be a feature set bolted onto ecommerce platforms. It will be the infrastructure beneath every interaction — from the moment a consumer expresses a preference to the moment a delivery is confirmed. AI-powered demand forecasting, dynamic pricing, personalized storefronts, automated customer service, and agentic checkout will be standard capabilities, not differentiators.

Early movers are already operationalizing this shift. Amazon and Walmart have embedded AI into real-time bidding, audience targeting, and campaign optimization. Instacart is deploying generative AI for personalized landing pages. Companies that delay this investment by even 18 months will find the capability gap functionally unbridgeable.

Shift 2: Social Commerce Becomes the Primary Discovery Engine

Social commerce is expected to grow three times faster than traditional ecommerce through 2025, with 70% of global consumers expecting to shop primarily through social media by 2030 — bypassing traditional websites entirely. This is not a marginal shift. It fundamentally changes where you must be visible, how you must present your brand, and what commerce capabilities your marketing infrastructure needs.

The winning model combines shoppable video content, creator partnerships, live commerce events, and seamless in-app checkout. Markets that are leading this shift — notably Southeast Asia, where TikTok drives 86% of online purchases in Thailand — offer a clear preview of where Western markets are heading.

Shift 3: Mobile-Native Architecture Becomes Non-Negotiable

Over 85% of Asian transactions are already mobile-initiated. US mobile commerce will reach $900 billion in 2025. By 2031, a company without a genuinely mobile-native experience — not a mobile-responsive website, but a purpose-built mobile interface — will be structurally disadvantaged in every market. This means progressive web apps, super-app integrations, voice-enabled search, and frictionless one-tap checkout.

Shift 4: Payments and Checkout Become a Competitive Moat

The payment layer is shifting from infrastructure to differentiation. Buy Now Pay Later transactions in the US reached $133 billion in 2024 and are projected to reach $206 billion by 2029. Digital wallets have climbed from 22% to 65% penetration in ecommerce transactions in the past decade. By 2030, digital payments will account for 79% of all ecommerce transactions.

Agentic checkout — where AI completes purchases autonomously — is the frontier. Businesses that integrate Stripe, open payment APIs, and AI-compatible checkout flows today are building a conversion advantage that will compound over the next five years.

Shift 5: Sustainability Becomes a Purchase Criterion, Not a Brand Position

Growing consumer awareness of environmental issues is driving measurable purchasing behavior, not just stated preferences. Ecommerce businesses that adopt eco-friendly packaging, carbon-neutral shipping, verified sustainable supply chains, and circular commerce models will attract the loyalty of the consumer segment — particularly Gen Z and Millennials — that will be the majority of purchasing power by 2031.

This is not optional philanthropy. It is a strategic positioning decision with quantifiable revenue implications.

Section 3: Five Strategic Imperatives

Based on the market analysis above, the following five imperatives represent the minimum set of structural commitments required to compete effectively in the 2031 ecommerce landscape. They are sequenced in order of both urgency and foundational dependency — each enables the next.

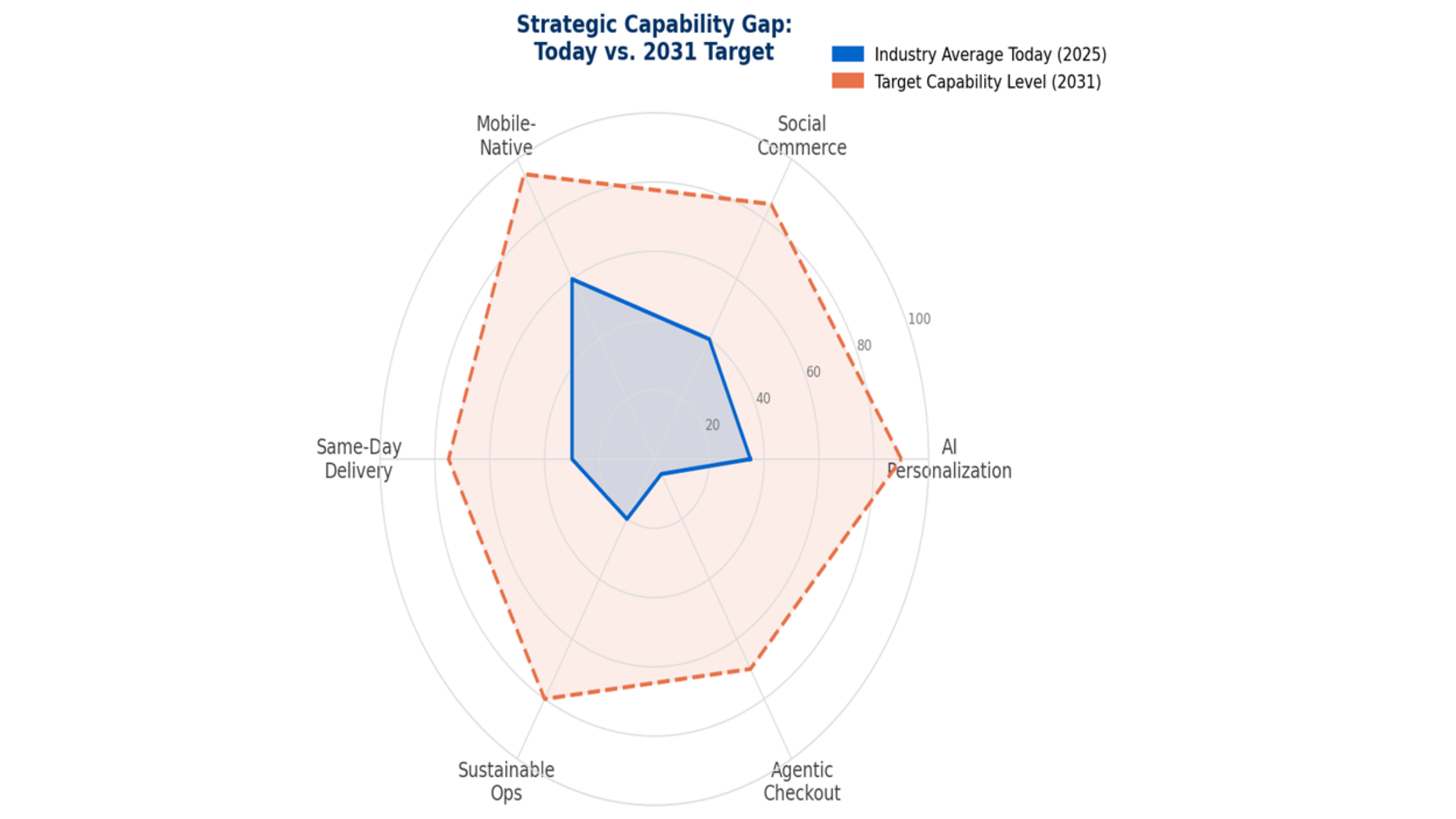

| Priority Area | Where You Are Today | Where You Must Be by 2031 |

| Channel Mix | Website + marketplace-first | Omnichannel: social, voice, in-app, D2C |

| Personalization | Segment-based campaigns | AI-driven 1:1 hyper-personalization at scale |

| Mobile Experience | Responsive website | Mobile-native, super-app or seamless PWA |

| Payments | Cards + basic digital wallets | BNPL, UPI-style instant pay, agentic checkout |

| Data & Analytics | Backward-looking reports | Predictive + prescriptive intelligence |

| Logistics | Standard delivery SLAs | Same-day, Q-commerce, automated last mile |

| Customer Service | Human-led support | AI agents handling 60–80% of interactions |

| Sustainability | Optional / PR-led | Core to brand promise, verified supply chain |

Imperative 1: Build a Unified Data Foundation

Every other strategic investment depends on this one. AI personalization requires clean, unified customer data. Omnichannel attribution requires integrated data pipelines across every touchpoint. Predictive analytics requires historical depth and real-time signals combined.

The priority action is consolidating your customer data platform (CDP), ensuring every interaction — web, app, social, in-store — feeds a single behavioral record per customer. This is the infrastructure on which all future capability is built.

Imperative 2: Activate AI-Driven Personalization

Personalization is the primary lever for conversion efficiency in a declining-conversion-rate environment. AI-driven personalization — product recommendations, dynamic pricing, personalized email and push, individualized search results — has demonstrated 10–12% average revenue lifts in businesses that have fully operationalized it.

The near-term target: ensure that AI recommendations account for at least 15–20% of revenue by end of 2027. The medium-term target: deploy AI for customer service automation, reducing human-handled interactions by 40–60% while maintaining or improving CSAT.

Imperative 3: Redesign for Omnichannel Commerce

The consumer does not think in channels. They think in moments. Your operational architecture must reflect that reality — a single inventory view, unified fulfillment, consistent pricing across touchpoints, and measurement that reports on the customer journey, not on individual channel performance in isolation.

This means activating social commerce on at least TikTok and Instagram with in-app checkout, building or acquiring same-day delivery capability in your top revenue markets, and implementing attribution models that give accurate credit across the full funnel.

Imperative 4: Engineer the Mobile Experience

Commission a full audit of your mobile conversion funnel. Identify every step where drop-off occurs and rebuild it with mobile-native interaction patterns — not adapted desktop patterns. Integrate one-tap checkout. Optimize for voice search. Consider whether a progressive web app or dedicated mobile app serves your specific customer base more effectively.

The benchmark: your mobile conversion rate should reach parity with desktop within 18 months. If it cannot, the problem is structural, not executional.

Imperative 5: Embed Sustainability into Operations

Begin with measurement: calculate the carbon footprint of your fulfillment operations, packaging materials, and product returns. Set public, time-bound reduction targets. Launch a returns-reduction initiative using better fit guidance, AR try-on, or clear size data.

Over the five-year horizon, the companies that will have a genuine sustainability story will be those that started building it in 2025–2026, not those that announce it in 2030.

Section 4: Execution Roadmap to 2031

The strategic imperatives above require coordinated execution across technology, operations, marketing, and leadership. The following phased roadmap provides a practical sequencing framework.

| Phase | Timeline | Key Initiatives | Success Metrics |

| Foundation Sprint | 2025–2026 | Unify data infrastructure; Mobile-first redesign; Activate 1–2 new social commerce channels | Data platform live; Mobile conversion +20%; First social revenue |

| Growth Acceleration | 2026–2028 | Deploy AI personalization; Launch D2C or subscription tier; Build same-day delivery in top markets | AI rec. revenue share >15%; Subscriber base; Delivery NPS >70 |

| Market Leadership | 2028–2031 | Agentic commerce integration; Expand cross-border; Embed sustainability metrics in every SKU | AI-assisted checkout share >30%; International revenue >25% |

Critical Success Factors

Executing this roadmap will require discipline in three areas that are often treated as secondary:

- Leadership alignment: The shift from channel-centric to customer-centric operations crosses functional boundaries. It requires C-suite ownership, not delegation to individual channel teams.

- Talent and capability: AI-native commerce requires new roles — data scientists, AI product managers, social commerce strategists. Begin recruiting and building these capabilities now. The competition for this talent will intensify significantly over the next 24 months.

- Technology investment governance: Resist the temptation to layer point solutions onto legacy architecture. A phased platform modernization that builds toward composable, API-first commerce infrastructure will out-perform short-term tactical fixes at scale.

Conclusion

The global ecommerce market is at an inflection point. The forces that drove the first era of online retail — connectivity, convenience, and product breadth — are now table stakes. The forces that will define the next era — intelligence, integration, and genuine consumer trust — are being built today by the companies that will lead it.

The trajectory is clear: a $6.86 trillion market in 2025 growing toward $11–13 trillion by 2031, with social commerce, AI-native operations, and mobile-first experiences reshaping the entire competitive landscape. The market will grow. The question is which companies will capture that growth and which will watch it accrue to faster-moving competitors.

The five imperatives in this report — unified data, AI personalization, omnichannel activation, mobile-native design, and sustainable operations — are not aspirational. They are the structural requirements for competing in the market that is being built right now.

The window to act is open. It will not remain open indefinitely.

| Key Takeaways

▸ Global ecommerce will exceed $11T by 2031. Social commerce will reach $6.2T alone. ▸ AI, mobile-native experience, and social commerce are structural shifts, not trends. ▸ Companies that build the five strategic capabilities now will disproportionately capture growth. ▸ The execution window is 2025–2027. Leaders are already moving. |

Sources & Methodology

This report draws on publicly available market data from eMarketer, Statista, Shopify Enterprise Research, DHL E-Commerce Trends Report 2025, Gartner Digital Commerce Research, DataHorizon Research, Capital One Shopping Research, SellersCommerce, Shoptrial, and Triple Whale. All statistics reference 2024–2025 data points unless otherwise noted. Projections are based on available CAGR data and multiple source triangulation. This document is intended for strategic planning purposes and does not constitute investment advice.

Leave A Comment